Forecasts reveal that COVID-19 will lead to economic losses in East Asia and the Pacific.

The region of East Asia and the Pacific (EAP) are expected to suffer heavy losses in their gross domestic product (GDP) for the year 2020, according to the April 2020 regional report released by the World Bank Group.

The COVID-19 pandemic which originated from China has led not only to a public health crisis but also resulted in a shock in supply and demand for the developing countries in EAP. World Bank’s forecasts suggest that this might push some of them into recession.

The vulnerable

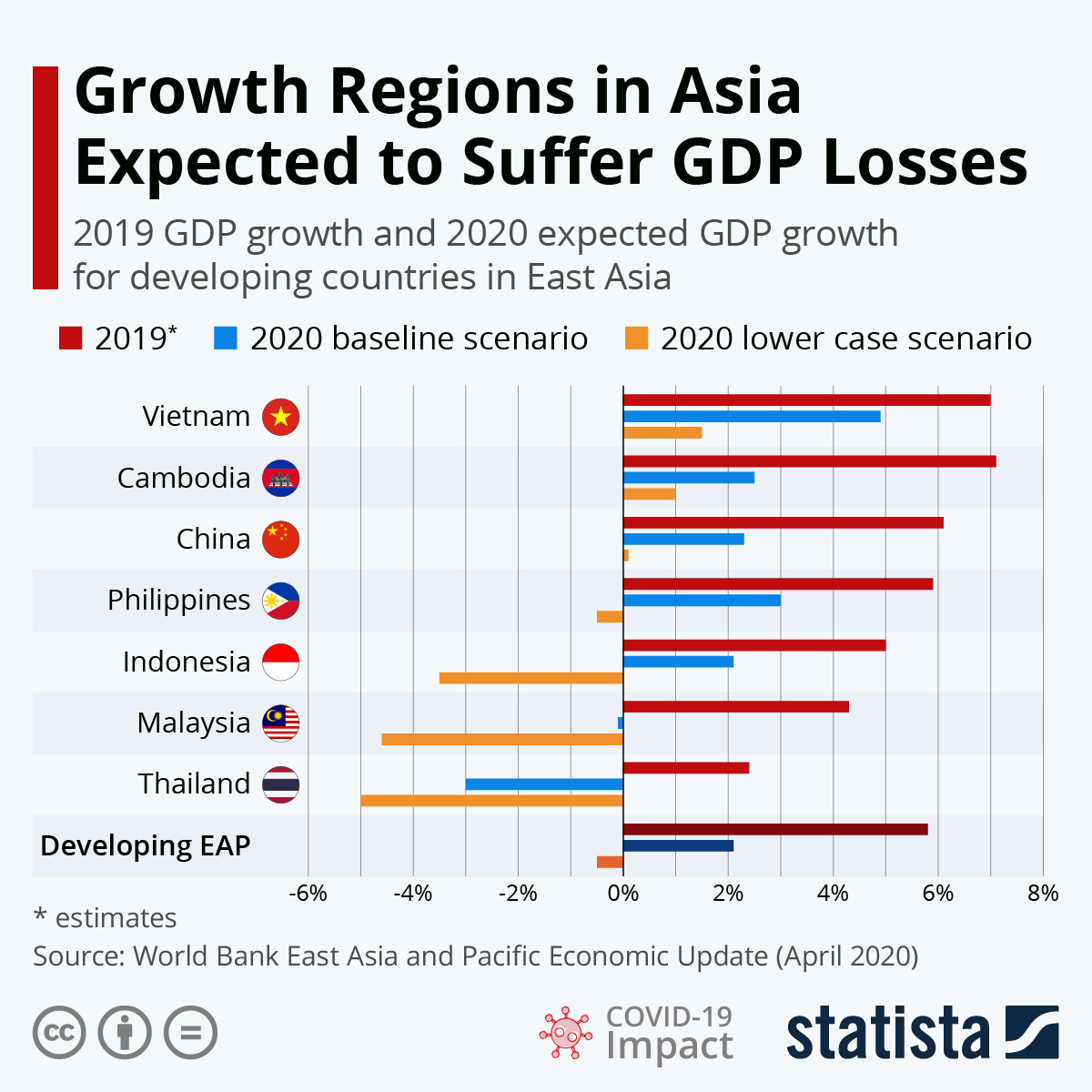

Thailand is expected to suffer the biggest GDP loss in 2020, with a loss in the 2020 GDP ranging from 3% to as high as 5% for the best-case and the worst-case scenario, respectively.

This is in stark contrast to 2019 where Thailand experienced a 2.4% growth. This means that the magnitude of the decrease in growth from 2019 can amount to as high as 7.4 percentage points all in all.

The vulnerability of Thailand in this pandemic is a mixture of its reliance on the tourism industry for its revenue — among the most affected industries during this crisis — as well as its high levels of national debt.

Another country expected to experience losses in their GDP for both the best- and worst-case scenario forecasts is Malaysia, with its 2020 GDP loss ranging from 0.1% to 4.6%.

In the worst -ase scenario, Philippines (-0.5%) and Indonesia (-3.5%) are expected to experience 2020 GDP declines. However, if they manage to recover quickly, the forecasts suggest that they can still attain some growth for this year.

Marginal growth

All countries in EAP are expected to experience declines in the growth rate of their GDPs, however, some countries will still experience growth, albeit marginal.

Cambodia is forecasted to gain one percent growth in GDP in the worst-case scenario. In the ideal outcome, this can go a bit higher at 2.5% percent. Even then, this is a huge decline from last year’s growth of 7.1%.

Similarly, Vietnam’s GDP is expected to grow at a rate of at least 1.5%. This can go slightly higher to 4.9% in the ideal scenario.

Even for these two countries, poverty risk remains high, especially for those in the most exposed sectors such as manufacturing and retail.

The economic giant China itself is expected to slow down. In the worst-case scenario, it will register a measly 0.1% growth which can go up to 2.3% if they recover quickly.

For the 2020 Q1, China already took a massive blow in its economy due to the pandemic, registering a decline in their GDP for the first time after more than 40 years.

We can see that no one is truly safe from the shock resulting from the COVID-19 pandemic. With this, there is a need for a substantial effort and strong policy from governments in order to soften the blow.